|

Showing posts with label election. Show all posts

Showing posts with label election. Show all posts

Friday, December 19, 2014

I'm Your Realtor and I Vote!

Monday, November 3, 2014

Lower Your Federal Taxes, Every Year, For the Life of Your Loan

Maryland HomeCredit Program

Lower Your Federal Taxes, Every Year, For the Life of Your Loan

A Maryland HomeCredit can save a homebuyer tens of thousands of dollars over the life of a home loan, and makes owning a home more affordable. Together with a home loan through the Maryland Department of Housing and Community Development's (DHCD's) Maryland Mortgage Program (MMP), which offers Down Payment Assistance and the certainty of a 30-year fixed interest rate, the State of Maryland is making the dream of sustainable homeownership a reality for more Marylanders than ever.

To get started, contact one of our approved MD HomeCredit lending partners today.

You may already know about the mortgage interest deduction that most homeowners already claim each year on their federal taxes. The Maryland HomeCredit Program is different, and provides a federal tax credit to eligible homebuyers. A tax deduction reduces the homeowner’s “taxable income”. In contrast, a tax credit, such as the Maryland HomeCredit, provides the homeowner with a reduction in their actual federal tax liability.

DHCD's Maryland HomeCredit Program provides eligible homebuyers with a federal tax credit that may be claimed annually, the value of which is equal to 25% of the value of mortgage interest payments (up to $2,000) paid each year, for the life of the loan (i.e. until payoff, sale, refinance or transfer).

How to Get a Maryland HomeCredit

Homebuyers apply for a Maryland HomeCredit through an approved mortgage lender. The Lender will confirm the borrowers' eligibility for this program, and submit an application to the Maryland Department of Housing and Community Development (DHCD).

Who Can Get a Maryland HomeCredit?

To get a HomeCredit, you must be purchasing a home in Maryland and meet borrowing criteria that include:

- You must meet the same income limits and home purchase price limits as the Maryland Mortgage Program;

- You cannot have owned a home during the past three (3) years, UNLESS you are purchasing in aTargeted Area;

- The home you purchase must be your primary residence.

NOTE - the Maryland HomeCredit Program is not available for refinances or existing homeowners

Calculating the Value of an Maryland HomeCredit

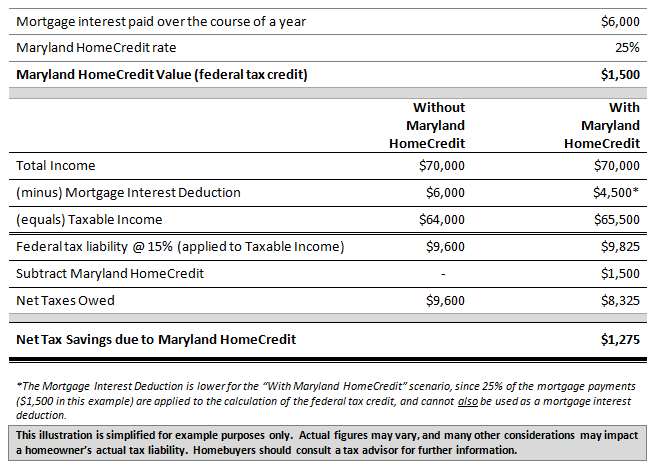

The size of the tax credit received by a homeowner with a HomeCredit is 25% of that year's mortgage interest payments, up to a maximum credit of $2,000 in any single year.

Note that the actual net savings due to the HomeCredit are likely to be less than the face value of the tax credit, since the value of the of interest payments associated with the tax credit (25% of total interest payments) cannot also be used as a standard mortgage interest deduction.

The following example shows a typical calculation:

Our downloadable calculator can help you estimate how a Maryland HomeCredit can provide you with savings over the life of a loan.

Maryland HomeCredit Fees

GET STARTED - Talk to an Approved Maryland HomeCredit Lender

Tuesday, August 14, 2012

Independent Foreclosure Review Fact Sheet

Independent Foreclosure Reviews

Fact Sheet

Independent Foreclosure Reviews

What is happening?

Fourteen U.S. mortgage servicers and their affiliates are making available free,

impartial Independent Foreclosure Reviews to certain of their borrowers as

part of the consent orders entered into with the Board of Governors of the

Federal Reserve System and the Office of the Comptroller of the Currency in

April 2011.

If eligible borrowers believe that they were financially injured as a result of

servicer errors, misrepresentations or other deficiencies in the foreclosure

process on their primary residence, they can request a review of their

foreclosure file to verify that their foreclosure process was handled properly.

Throughout this process, servicers will continue their efforts to help

homeowners who have not yet gone through a foreclosure sale stay in their

homes, where possible.

Who is eligible?

Borrowers are eligible to submit a Request for Review if 1) their loan was

serviced by one of the participating mortgage servicers, 2) their loan was active

in the foreclosure process between Jan. 1, 2009 and Dec. 31, 2010, and 3) the

property securing the loan was their primary residence.

To participate in an official review, eligible borrowers must submit a completed

Request for Review Form by April 30, 2012.

Which servicers are being required to perform the reviews?

The participating servicers are:

- America’s Servicing Company

- Aurora Loan Services

- BAC Home Loans Servicing

- Bank of America

- Countrywide

- EMC

- EverBank/Everhome Mortgage Company

- GMAC Mortgage

- HFC

- National City Mortgage

- PNC Mortgage

- Sovereign Bank

- SunTrust Mortgage

- U.S. Bank

- Beneficial

- Chase

- Citibank

- HSBC

- IndyMac Mortgage Services

- Wachovia

- Washington Mutual (WaMu)

- CitiFinancial

- MetLife Bank

- Wells Fargo

- CitiMortgage

- Wilshire Credit Corporation

How can borrowers find out if they are eligible for a review?

An estimated 4.5 million borrowers will be notified by a letter explaining the

review process and a Request for Review Form. The mailings will be

staggered—to better manage volumes—in stages beginning Nov. 1, 2011.

Information also may be found at www.IndependentForeclosureReview.com.

Borrowers who believe they may be eligible for a review who do not receive a

mailing can call 1.888.952.9105 Monday through Friday 8:00 a.m. – 10:00 p.m.

ET and Saturday 8:00 a.m. – 5:00 p.m. ET to determine if they are eligible.

What does it mean that a borrower was active in the foreclosure process?

Foreclosure actions include any of the following occurrences on a primary

residence between the dates of Jan. 1, 2009 and Dec. 31, 2010:

The property was sold due to a foreclosure judgment.

The mortgage loan was referred into the foreclosure process but was

removed from the process because payments were brought up-to-date or

the borrower entered a payment plan or modification program.

The mortgage loan was referred into the foreclosure process, but the

home was sold or the borrower participated in a short sale or chose a

deed-in-lieu or other program to avoid foreclosure.

The mortgage loan was referred into the foreclosure process and remains

delinquent but the foreclosure sale has not yet taken place.

What information will borrowers need to provide?

Borrowers will be asked to provide information on the property, the borrower

and any co-borrowers, and details about how they believe they may have been

financially injured. There is no charge to eligible borrowers for a review, which

will not be reported to any of the credit bureaus and will not impact any other

options a borrower may pursue related to their foreclosure.

What constitutes “financial injury?”

Listed below are examples of situations that may have led to financial injury.

This list does not include all situations.

The mortgage balance amount at the time of the foreclosure action was

more than you actually owed.

You were doing everything the modification agreement required, but the

foreclosure sale still happened.

The foreclosure action occurred while you were protected by bankruptcy.

You requested assistance/modification, submitted complete documents

on time, and were waiting for a decision when the foreclosure sale

occurred.

Fees charged or mortgage payments were inaccurately calculated,

processed, or applied.

The foreclosure action occurred on a mortgage that was obtained before

active duty military service began and while on active duty, or within 9

months after the active duty ended and the servicemember did not waive

his/her rights under the Servicemembers Civil Relief Act.

How long will the foreclosure review take to complete?

The borrower will be sent an acknowledgement letter from the Independent

Review Administrator within one week after the request is received. Because

the review process will be a thorough and complete examination of many

details and documents, a review could take up to several months.

Who will be conducting the reviews?

Foreclosure Reviews will be conducted by independent consultants engaged by

the servicers and approved by the Board of Governors of the Federal Reserve

System and the Office of the Comptroller of the Currency. In order to ensure

that the request for review process is as consistent as possible for eligible

customers, all of the participating servicers are using the same outside

administrator to manage the handling of incoming complaints for the Request

for Review process.

Once the Request for Review Forms have been collected by this single vendor,

the servicer will provide relevant documents to the independent consultant.

The servicer will also provide any findings and recommendations related to the

borrower’s request for review to the independent consultant for examination.

Servicers may be asked to clarify or confirm facts and disclose reasons for

events that occurred related to the foreclosure process, and customers could

be asked to provide additional information or documentation.

Friday, October 22, 2010

Your Vote DOES Count.

For the upcoming 2010 General Election, you have 7 days and 7 ways to cast your vote. Please pick a convenient option below and make sure that your vote is counted.

You Have 7 days to Vote in 2010 (Early Voting Days and General Election Voting Day):

1. Friday, October 22 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

2. Saturday, October 23 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

3. Monday, October 25 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

4. Tuesday, October 26 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

5. Wednesday, October 27 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

6. Thursday, October 28 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

7. Tuesday, November 2 - Hours: 7:00 a.m. – 8:00 p.m. (General Election Day - Vote must be cast at your assigned precinct)

You Have 7 Ways to Vote in 2010:

1. College Park Community Center - 5051 Pierce Ave., College Park, MD. 20740 (Early Voting Location)

2. Bowie Library - 15210 Annapolis Rd. , Bowie, MD. 20715 (Early Voting Location)

3. Upper Marlboro Community Center - 5400 Marlboro Race Track Rd Upper Marlboro, MD 20772 (Early Voting Location)

4. Wayne K. Curry Sports & Learning Center - 8001 Sheriff Rd., Landover, MD. 20785 (Early Voting Location)

5. Oxon Hill Library - 6200 Oxon Hill Rd., Oxon Hill, MD. 20745 (Early Voting Location)

6. Your Assigned Precinct (Vote at your home precinct on Tuesday, November 2, 2010)

7. Vote by Mail (Complete the attached Absentee Application no later than Tuesday, October 26, 2010)

Please share and forward this message to your family, friends and neighbors. Prince George’s County is the battleground for this election. We have to make sure that President Barack Obama has a Democratic Governor and Democratic members of Congress from Maryland. We must make sure that our voice is heard and that Our Vote Counts!

You Have 7 days to Vote in 2010 (Early Voting Days and General Election Voting Day):

1. Friday, October 22 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

2. Saturday, October 23 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

3. Monday, October 25 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

4. Tuesday, October 26 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

5. Wednesday, October 27 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

6. Thursday, October 28 - Hours: 10:00 a.m. – 8:00 p.m. (Must vote at one of the early voting locations listed below)

7. Tuesday, November 2 - Hours: 7:00 a.m. – 8:00 p.m. (General Election Day - Vote must be cast at your assigned precinct)

You Have 7 Ways to Vote in 2010:

1. College Park Community Center - 5051 Pierce Ave., College Park, MD. 20740 (Early Voting Location)

2. Bowie Library - 15210 Annapolis Rd. , Bowie, MD. 20715 (Early Voting Location)

3. Upper Marlboro Community Center - 5400 Marlboro Race Track Rd Upper Marlboro, MD 20772 (Early Voting Location)

4. Wayne K. Curry Sports & Learning Center - 8001 Sheriff Rd., Landover, MD. 20785 (Early Voting Location)

5. Oxon Hill Library - 6200 Oxon Hill Rd., Oxon Hill, MD. 20745 (Early Voting Location)

6. Your Assigned Precinct (Vote at your home precinct on Tuesday, November 2, 2010)

7. Vote by Mail (Complete the attached Absentee Application no later than Tuesday, October 26, 2010)

Please share and forward this message to your family, friends and neighbors. Prince George’s County is the battleground for this election. We have to make sure that President Barack Obama has a Democratic Governor and Democratic members of Congress from Maryland. We must make sure that our voice is heard and that Our Vote Counts!

Subscribe to:

Posts (Atom)